How Vertical Drama Makes Money: Inside the Microdrama Business Model

Vertical drama generated $11B globally in 2025. A breakdown of episode unlocks, subscriptions, IAP models, Meta vs TikTok ad spend, co-production deals, and what creators actually earn.

The microdrama business model is built on one mechanic: give the first episodes away free, then charge to continue. Vertical drama apps generated over $11 billion globally in 2025. Through episode unlocks, subscriptions, in-app purchases, and performance marketing at a scale most of the traditional entertainment industry still hasn't fully processed.

How Vertical Drama Platforms Make Money: Three Models

-The Episode Unlock

The foundation is simple. The first 5–10 episodes of any series are free. Then the viewer hits a paywall, placed at the moment of maximum unresolved tension, where emotional investment is highest and walking away feels costly.

At that point, the viewer makes a decision: unlock the next episode, buy the full series, subscribe for unlimited access, or leave. Scripts are written around this moment. Paywall placement is not a post-production decision. It shapes episode structure from the first draft. The narrative serves the monetization.

-IAP - In-App Purchase

In-app purchase dominates in high-income markets, particularly the U.S. Users buy virtual currency, coins, keys, gems depending on the platform, and spend it to unlock individual episodes or full series. A single episode runs $0.30–$0.50. A full series bundle is typically $10–$15. Most platforms also offer weekly, monthly or annual subscriptions, some all-access passes run $200 per year, for heavy users who prefer to remove the friction entirely.

Revenue is concentrated. A small segment of users spending over $100 per month drives most of the income. Vertical drama operators borrow the term "whales" directly from mobile gaming. The comparison is deliberate, and accurate.

-IAA - In-App Advertising

Ad-supported models dominate in price-sensitive markets: Southeast Asia, Latin America, parts of Europe. Content is free; revenue comes from ads served between episodes or as rewarded unlocks, where a viewer watches an ad instead of paying. ARPU is significantly lower than IAP markets, sometimes by a factor of five or six. But audience scale is larger. Most platforms use IAA as the entry strategy in new geographies, then layer conversion mechanics on top.

-IAAP - Hybrid

The hybrid is where the market is converging. Free episodes, episodic paywalls, rewarded ads, and optional subscription tiers, all within a single platform, monetizing different audience segments differently.

China completed this transition first. The market shifted from pure IAP toward ad-supported scale, with IAA now accounting for more than half of Chinese market revenue. International platforms are running the same arc, compressed into a shorter timeframe.

ARPU vs ARPPU: The Number That Actually Matters

Traditional streaming analysis uses ARPU across a broad subscriber base. Vertical drama runs on ARPPU, average revenue per paying user, because most viewers never pay anything.

The more strategically important metric is lifetime user value by geography. A U.S. user is estimated to be worth up to six times more over their lifetime than users in other markets. This is why platforms spend aggressively to acquire American audiences despite higher CAC. The math justifies it. The U.S. market generated approximately $1.3 billion in vertical drama revenue in 2025.

YouTube: The Long Game

A less-discussed revenue stream is YouTube. Not for direct series monetization, but as a long-term audience and ad revenue engine. Several Chinese-backed platforms and larger production companies maintain YouTube channels publishing full episodes or curated clips, monetizing through YouTube's ad-share system.

It's a slower, lower-margin play than IAP. But it builds search-indexed content libraries that compound over time and captures audiences who would never pay for in-app unlocks. For productions that own their IP outright, YouTube becomes a passive revenue layer that keeps generating income long after a series stops being actively promoted.

Co-Production: MG + Waterfall

As the market matures, more platforms are opening co-production arrangements with independent studios, moving beyond pure content acquisition toward shared risk and shared upside.

The prevailing structure is a minimum guarantee (MG) plus waterfall revenue share. The platform commits a minimum payment against future performance. Once revenue crosses defined thresholds, the production partner receives a share of upside. Both the MG and the waterfall percentages vary considerably. Deal terms differ by platform, territory, content genre, and the production company's track record. There is no industry standard yet. Opacity remains the norm.

✱

Here's how the money actually works, on both sides of the equation.

Join Real Reel

Where the Money Goes: Marketing Costs in Vertical Drama

At MIP London in early 2026, platform executives were unusually candid about where platform money actually goes. Some indicated that as much as 90% of total budget allocation goes toward marketing and user acquisition, not content. A series costing $200,000 to produce might sit inside a $2 million promotional campaign.

→ Real Reel reported on the MIP London economics discussion:

In conventional entertainment, content is the product. Marketing supports it. In vertical drama, content is the conversion asset. The marketing operation is the business. The relevant comparators are not Netflix or HBO. They are mobile gaming portfolios, where a small number of high-performing titles subsidize a large slate of experiments, and where data drives every decision.

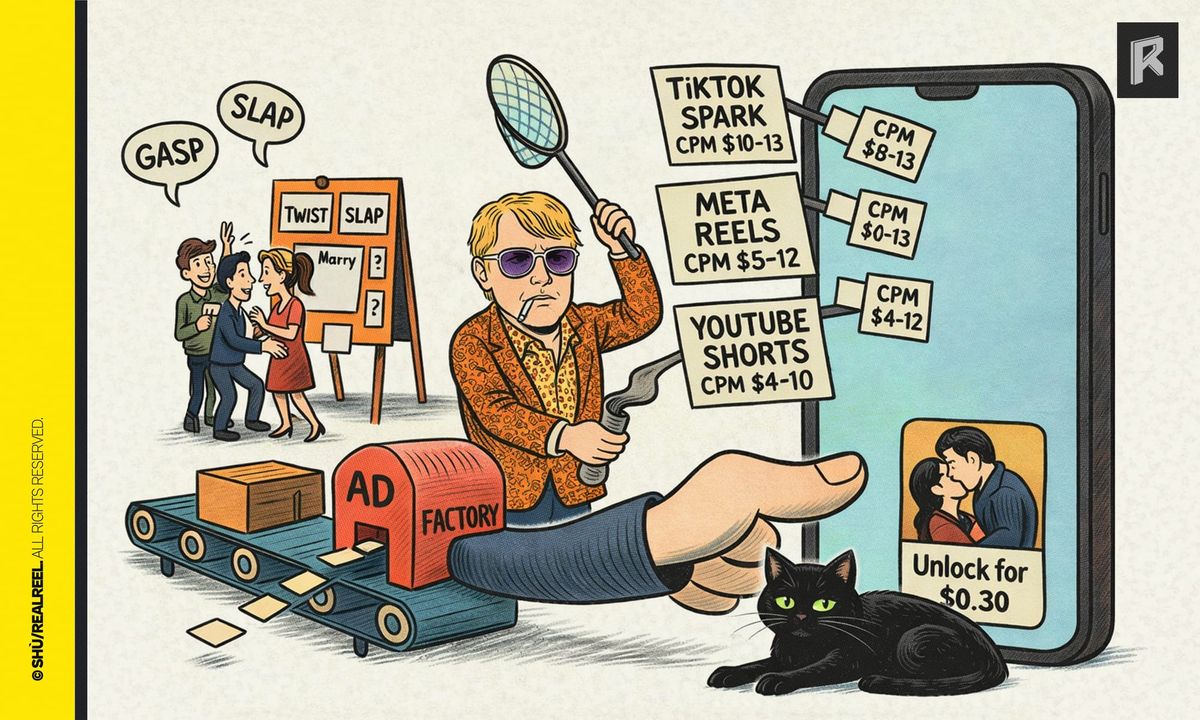

Meta vs TikTok: Where the Spend Actually Goes

Performance marketing for vertical drama concentrates on two platforms.

Meta (Facebook and Instagram) is the dominant channel for user acquisition in English-speaking markets. CPMs run $5–$12. More importantly, operator feedback consistently points to higher return on ad spend from Meta than from TikTok. Conversion rates, particularly for the core female 30–55 demographic that drives most platform revenue, have proven more reliable on Meta.

TikTok matters for discovery and reach. North American CPMs run $10–$13, and algorithmic amplification for content that performs organically is real. Spark Ads, which boost organic clips rather than separate ad creative, are now a standard tool. But conversion from TikTok to paying user runs lower than Meta for most established platforms. The gap narrows for certain genres and younger audience segments, but the pattern holds.

YouTube and Google AdMob play supporting roles. YouTube pre-roll and Shorts for awareness, AdMob for reaching audiences inside other apps. CPMs are lower ($4–$10 for YouTube), but targeting is different enough to justify inclusion in a full-funnel strategy.

→ For how this marketing logic shapes what gets written into vertical drama scripts:

How Creators and Production Partners Get Paid

The least transparent part of vertical drama economics has historically been what creators actually earn. That is beginning to shift.

Vigloo launched its Vigloo Studio Dashboard, a creator analytics system giving production partners direct access to viewership data, episode completion rates, geographic performance, and estimated revenue insights, with AI-generated audience analysis layered on top. For an industry where platforms have traditionally controlled all the data, this is a meaningful change. Platforms that offer data transparency are starting to compete on that dimension as a way to attract better production talent.

→ More in our weekly info:

muVpix, the platform launched by actor and filmmaker John Lewis, has made creator-friendly economics a core part of its positioning, building transparent revenue-sharing structures as a differentiator against platforms where earnings visibility is limited. Lewis put the economics plainly in his conversation with Real Reel: "A vertical series might cost a few hundred thousand dollars to produce and market. If it performs reasonably well, it can generate a few million. If it performs extremely well, it can generate much more than that. That spread between production cost and revenue potential is very different from traditional filmmaking."

→ More thought the R:ID interview with muVpix founder John Lewis:

→ More in our weekly info:

The direction is clear. As the production talent pool becomes more selective about where it takes work, data transparency and fair revenue sharing will become competitive advantages, not just ethical considerations.

What the Numbers Actually Look Like

Platform profitability is rarely disclosed cleanly. The available data:

DramaBox reported $323 million in revenue and $10 million in net profit in 2024, one of the few platforms to disclose a profitable year at scale. ReelShort generated approximately $400 million in 2024 revenue but is widely believed to remain loss-making due to aggressive user acquisition spend. Deliberate choice: market share over margin. Q1 2025 global in-app purchase revenue across vertical drama apps approached $700 million, roughly four times the equivalent quarter in 2024.

The profitability picture makes more sense through the mobile gaming lens. Early-stage platforms prioritize scale and habit formation over margin, accepting losses on CAC in exchange for audience lock-in. The bet is that once users are spending 35+ minutes a day on the app, monetization efficiency can be improved over time. China's mature market suggests it can. International markets are still proving it.

→ For the full analysis of how China's market completed the structural cycle first:

FAQ

What is the microdrama business model?

The microdrama business model combines free content with episodic paywalls, monetizing viewer engagement through in-app purchases, advertising, and hybrid unlock mechanics rather than monthly subscriptions.

How do microdrama apps make money?

Through a combination of in-app purchases (virtual currency to unlock episodes), monthly or annual subscriptions, and advertising. Most mature platforms offer all three, letting different audience segments monetize differently, casual viewers through ads, engaged viewers through episode unlocks, and heavy users through subscriptions.

How much does it cost to unlock a vertical drama episode?

Typically $0.30–$0.50 per episode individually. Full series unlocks range from $8–$15 depending on the platform and episode count.

What is ARPPU in vertical drama?

Average revenue per paying user. More meaningful than ARPU across total users, because most viewers never pay. The lifetime value of a U.S. paying user is estimated at up to six times the international average, which is why platforms spend disproportionately to acquire American audiences.

Do vertical drama platforms share revenue with creators?

Deal terms vary widely. Co-production arrangements typically involve a minimum guarantee plus waterfall revenue share, but both figures are negotiated case by case. Data transparency is improving. Vigloo's Studio Dashboard is one example of platforms beginning to open performance data directly to production partners.

Meta or TikTok: which works better for vertical drama advertising?

Both are used, but operator feedback consistently points to higher return on ad spend from Meta, particularly for the core female 30–55 demographic. TikTok is more effective for reach and organic amplification. Most platforms run Meta as the primary conversion engine and TikTok as the awareness layer.

Is vertical drama profitable?

Depends on the platform. DramaBox reported $10M net profit on $323M revenue in 2024. ReelShort at higher revenue scale is believed to remain loss-making due to user acquisition investment. Profitability is a function of CAC efficiency and audience lifetime value, not just revenue scale.

For the bigger picture on how vertical drama's economics are reshaping streaming:

For a complete overview of the format, platforms, and global market:

✱