How Vertical Drama Is Changing Streaming Economics

Microdrama apps have overtaken Netflix in daily mobile engagement. Here's what vertical drama's economics actually look like, and why streaming can't ignore the logic anymore.

March 2026

This is an original Real Reel OBS research editorial.

Unauthorized reproduction, redistribution, or commercial use is prohibited without prior written permission. Brief quotations are permitted with clear attribution.

Vertical drama is reshaping the economics of streaming. Microdrama platforms, led by ReelShort, DramaBox and a growing field of mobile-native apps, have surpassed Netflix and Disney+ in daily mobile engagement time, according to Omdia's Q4 2025 data. With global microdrama revenue reaching an estimated $11 billion in 2025 and projected to hit $14 billion in 2026, the vertical video format is no longer a niche experiment. It is a parallel entertainment economy, running on different monetization logic, different production assumptions, and different ideas about what audiences will pay for.

✱

The question is no longer whether vertical drama can compete with streaming. It already has, on the metric that matters most: ATTENTION.

Join Real Reel

When Omdia released its Q4 2025 mobile engagement data in February, the numbers landed differently than usual vertical drama coverage. This wasn't a trade publication writing about a niche format finding its footing. This was a major research firm saying, with hard data, that microdrama apps had surpassed Netflix, Disney+ and Amazon Prime Video in daily mobile viewing time in the United States. ReelShort users were spending 35.7 minutes a day on the app. Netflix clocked 24.8 minutes. Disney+ came in at 23.

Netflix still leads in overall monthly users by a wide margin. But engagement intensity tells a different story about where mobile habit is actually forming, and habits are what monetization runs on.

This isn't the same argument as "vertical drama will replace streaming." It's a more specific one: vertical drama has introduced a different economic logic into the video entertainment landscape, one that runs on different incentives and doesn't need to win the subscriber war to reshape how the broader industry allocates capital.

The economic inversion that conventional streaming hasn't solved

Traditional streaming platforms are built on one premise: the subscription. Content is produced to reduce churn, attract new members, and justify the monthly fee. Revenue is predictable. The creative mandate is essentially prestige: make shows people talk about and keep them subscribed.

The structural problem is that subscription economics require continuous investment in premium content to defend an existing membership base while also growing it. When subscriber growth plateaus, the model starts to strain.

Netflix is profitable, but that profitability now depends increasingly on monetizing the existing base more aggressively through ad tiers and price increases, not on adding new subscribers the way it once did.

Vertical drama arrived with a different answer. Rather than building subscriber relationships, it built conversion machines.

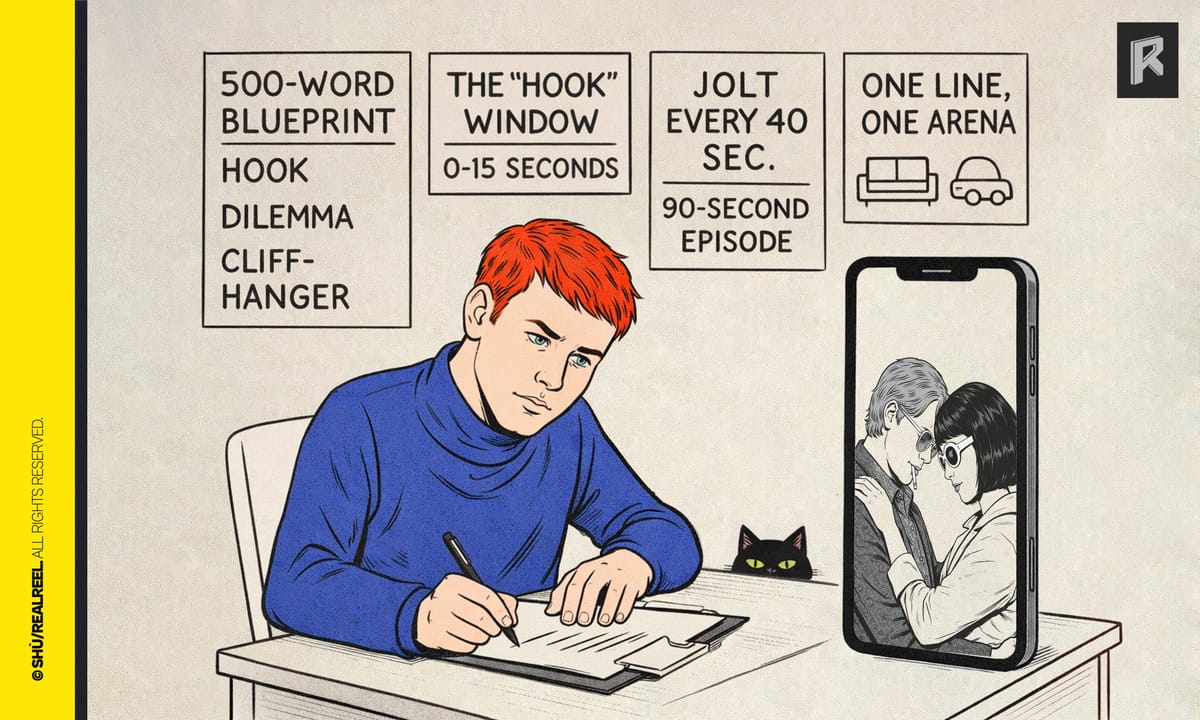

As we laid out in the Real Reel Industry Guide, vertical drama's defining economic feature is that monetization is not downstream of storytelling. It's upstream. Episodes are written around cliff placement. Release cadence is engineered to maximize how often a viewer hits a paywall, which is the moment when a free episode ends and the next one costs something. The narrative serves the revenue mechanics, not the other way around. That's not a criticism of the format. It's a structural description of why it competes so differently.

The revenue model reflects this too. Traditional streaming runs on ARPU (average revenue per user) spread across a large subscriber base paying a flat monthly fee. Vertical drama runs on ARPPU (average revenue per paying user) and the numbers look very different. A small but highly engaged segment of users will spend over $100 a month unlocking episodes. Across platforms, the majority of revenue comes not from advertising but from direct user payments through microtransactions. The model resembles mobile gaming far more than it resembles Netflix.

If you want to go deeper on how the business model actually works:

What $11 billion actually means and what it doesn't

Omdia puts global microdrama revenue at roughly $11 billion in 2025, heading toward $14 billion in 2026 ↗. About $3 billion of that is outside China, with the U.S. expected to represent close to half of the non-China market next year.

For context: Netflix did around $45 billion in revenue last year. The U.S. box office was about $8.9 billion. Vertical drama is still a fraction of the long-form streaming economy and probably will be for a while.

But the scale comparison misses the point. The trajectory is what matters.

In China, vertical drama went from roughly $500 million in 2021 to over $7 billion by 2024. Last year, Chinese microdrama revenues surpassed the country's domestic theatrical box office for the first time. What traditional streaming took a decade to prove, that mobile-first, serialized, paid content could actually scale, vertical drama demonstrated in China in under four years, with a fraction of the production budget and none of the prestige infrastructure. International markets are earlier in that cycle. But the cycle is underway. Microdrama app downloads surged past 2.3 billion globally in 2025, more than doubling year over year, while traditional streaming app downloads fell more than 4%.

That divergence doesn't feel accidental.

The 90% Marketing Problem: Where Microdrama Money Actually Goes

Maybe the most clarifying data point from early 2026 didn't come from a research report. It came from a panel at MIP London, where executives were unusually candid about where platform money actually goes. Some said as much as 90% of total budget can go toward marketing and user acquisition, not content.

The comparison made repeatedly in those conversations was to mobile gaming: funnel optimization, conversion mechanics, data-driven retention.

This is disorienting if you're trained in traditional media economics, where content is the product and marketing supports it.

In vertical drama, that relationship is inverted.

Content is the hook. The marketing operation is the actual business.

It has a direct implication for how this industry should be analyzed. The relevant comparators aren't really other content companies. They're mobile gaming portfolios, performance marketing operations, subscription management businesses.

Once you understand that content is functioning as a conversion asset rather than a prestige one, a lot of vertical drama's production logic stops looking like corner-cutting and starts looking like rational engineering.

Which is also what the anatomy of a vertical drama script actually looks like when you examine it closely. The writing choices that seem cheap or formulaic from a film school perspective are often deliberate retention mechanics.

If you want to see what that looks like at the script level:

Hollywood Is No Longer Watching From a Distance

For most of vertical drama's early growth, Hollywood watched from a distance. The aesthetic, the unknown talent, the misalignment with subscription logic all made it easy to dismiss.

That's visibly changing now.

Fox Entertainment took an equity stake in Holywater, the company behind the My Drama app, with a commitment to producing over 200 shows for the platform. CSI creator Anthony Zuiker started writing for GammaTime. Google entered through a content partnership with Range Media, building a microdrama slate with veteran TV producers for the Google TV app. Disney+ launched "Verts," a vertical video feed inside its mobile app. Peacock began experimenting with vertical formats for sports.

These moves aren't all saying the same thing. Some represent genuine format commitment. Others are hedging.

But what's significant isn't any one of these decisions in isolation. It's that they're happening simultaneously. When major platforms start integrating vertical logic at the same time, even experimentally, the format's position in the entertainment economy shifts from challenger to something more structural.

The two systems aren't converging. But they're starting to acknowledge each other, which is a different kind of signal.

Some signals here:

The Distribution Gap: Why Traditional Sellers Are Being Cut Out

One of the clearest signs of vertical drama's structural maturity is where traditional industry infrastructure is conspicuously missing.

Major distributors have been slow to engage. Their existing sales models are built around long-form catalog, territory windowing, and relationships that don't map onto vertical drama's pace or volume. Chinese microdrama services are often commissioning directly from production partners and going straight to platforms, cutting out the distribution layer entirely.

That gap doesn't slow vertical drama down.

It concentrates value elsewhere: in the platforms that control commissioning, in the production partners that can sustain velocity, and in the operators who built the performance marketing infrastructure from scratch.

What's traveling internationally isn't just content. It's an operational system that was refined inside China's mature ecosystem over years. Localization pipelines, IP adaptation frameworks, rights licensing structures. The competitive moat being built isn't about individual titles. It's about infrastructure.

If you want to read our full analysis of how international markets are actually developing:

What Vertical Drama Is Actually Doing to Streaming Economics

To be precise about what vertical drama is doing to streaming economics, and what it isn't.

It's not replacing subscription video. Netflix's content investment and subscriber base remain dominant. Long-form prestige is still a viable business.

It is competing for mobile attention in a way that streaming platforms haven't successfully done. The Omdia engagement data is the most important signal here.

On mobile specifically, the distinction between winning on scale and winning on daily habit may erode faster than most streaming executives are planning for.

It is demonstrating a different monetization architecture. The IAP model, in-app purchases, meaning pay-per-episode unlocks where the cliffhanger is literally a payment prompt, has shown that audiences will pay for serialized content outside of subscription logic. That has implications for how platforms beyond vertical drama think about episodic monetization.

And it is accelerating capital reallocation. Once engagement data and revenue forecasts align at this scale, capital moves. Microdrama is no longer competing for cultural legitimacy. It's competing for mobile video budgets.

The underlying logic of the two systems is worth holding side by side for a moment. Traditional streaming optimizes for a long subscriber relationship: acquire a user, keep them subscribed, amortize content cost over time. Vertical drama optimizes for intensity within a session: hook the user immediately, escalate quickly, trigger a payment before they disengage.

One bets on loyalty. The other bets on urgency. Both work.

They just work on completely different assumptions about human behavior.

If you want the data behind that shift:

The structural question entering 2026

The streaming industry spent its first decade competing on content volume, then quality, then bundling and pricing. Vertical drama has opened a different front: monetization architecture.

The harder question for legacy platforms isn't whether to add a vertical feed. The interface is easy to copy. It's whether the underlying economic logic, performance marketing loops, episodic paywalls, portfolio-level risk management, content as a conversion tool, can actually be adopted by organizations built around different incentives, different talent relationships, different definitions of what success looks like.

For vertical drama, the question is whether the infrastructure layer can be built fast enough internationally to replicate what China's integrated ecosystem produced over a decade.

Neither question has a clean answer yet.

What is settled is the pressure.

Vertical drama has shown that mobile attention is contestable, that subscription isn't the only path to serialized monetization, and that narrative structure and revenue mechanics can be engineered together from the start.

That changes the economics.

Not just of vertical drama.

Of streaming itself.

✱